The History of Credit Counseling

Credit counseling in the United States grew alongside modern consumer credit. As installment credit and later revolving credit became part of everyday life after World War II, more households needed structured help dealing with missed payments, repayment strain, and the risk of bankruptcy.

This history traces how nonprofit credit counseling developed, how debt management plans became part of the field, and why disclosure standards, consumer protections, and oversight grew more important over time.

That background helps explain why nonprofit credit counseling works the way it does today and why it is important to distinguish it from debt settlement and other forms of debt relief.

It also gives consumers better context for evaluating a market in which many services may sound similar at first but operate very differently in practice.

At a glance

- Credit counseling grew alongside the expansion of modern consumer credit.

- Debt management plans were designed to help consumers repay over time, usually with creditor concessions.

- Fair share funding supported many agencies for decades while also raising questions about independence and incentives.

- Stronger regulation later helped separate nonprofit counseling from credit repair and debt settlement models.

How credit counseling began in the United States

In the decades following World War II, installment credit became more common in American life. Households increasingly used borrowed funds to purchase cars, appliances, and other major goods. Over time, revolving credit expanded as well, giving consumers broader and more continuous access to borrowing than earlier generations typically had.

As credit became more available, financial strain became more visible. More households faced delinquency, default, collection pressure, and the possibility of bankruptcy. That created a practical need for more structured ways to respond when consumers became overextended.

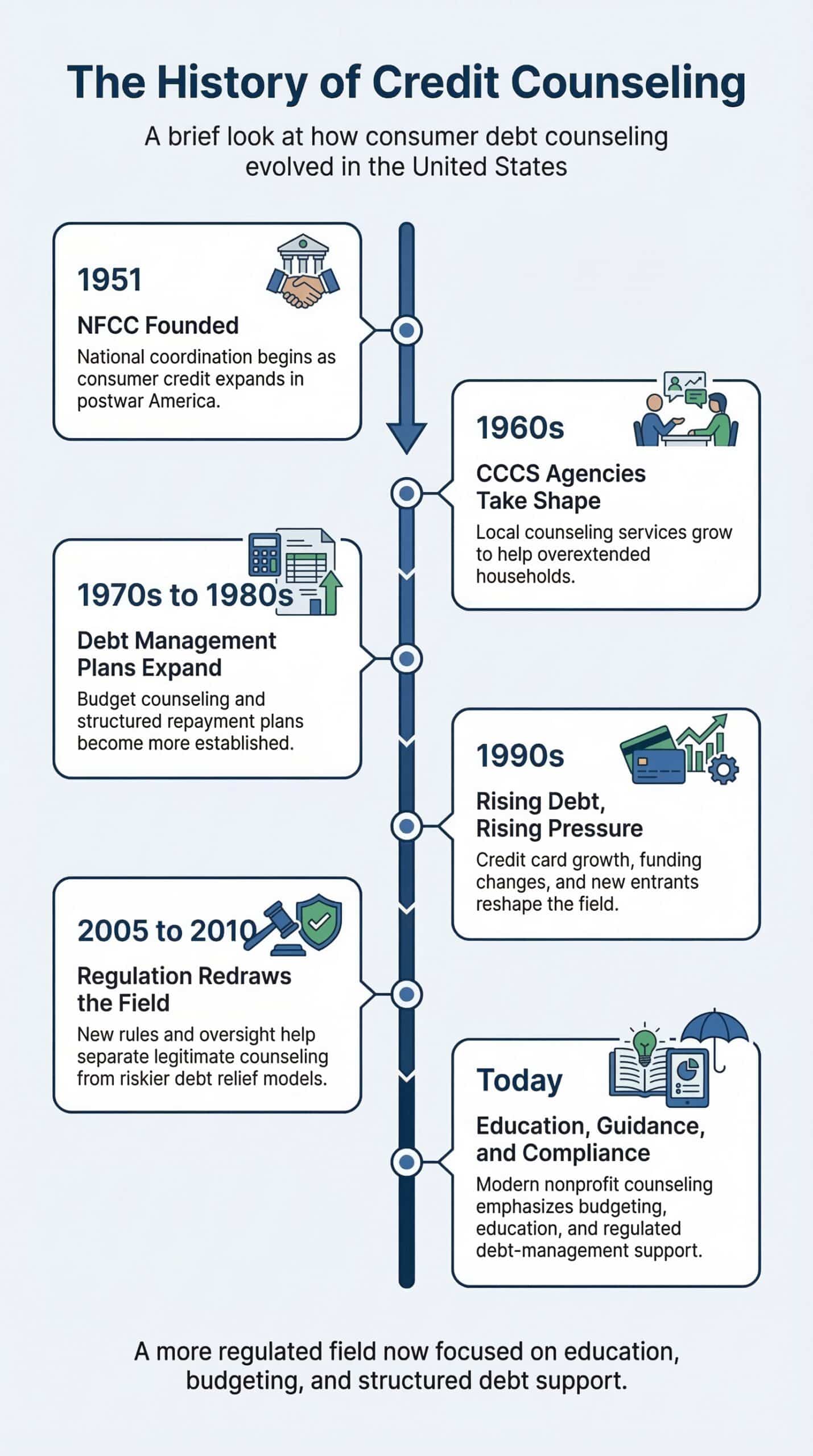

Organized credit counseling took shape in the 1960s, largely through efforts by department store credit managers and community-based nonprofit agencies seeking more coordinated ways to help consumers who were falling behind. One important national institution in that history was the National Foundation for Consumer Credit, founded in 1951 and later renamed the National Foundation for Credit Counseling.

From the beginning, credit counseling was shaped by both consumer need and creditor interests. It was designed to provide guidance and structure to households under stress, but it also developed inside a credit system that had a clear interest in improving repayment and limiting losses.

The rise of fair share and debt management plans

One of the industry’s defining developments was the debt management plan, often called a DMP. A traditional DMP is not a new loan and it is not a settlement agreement. Instead, it is a structured repayment arrangement in which a consumer makes one monthly payment through a counseling agency, and the agency distributes those funds to participating creditors.

In many cases, creditors agreed to concessions that made repayment more workable. Those concessions often included reduced interest rates, waived late fees, or other modified terms. In a traditional DMP, however, the consumer generally continued repaying the full principal balance over time.

For many years, counseling agencies were also supported through a voluntary creditor funding model known as fair share. Under fair share, participating creditors returned a percentage of recovered funds to counseling agencies. Early rates often ranged from 15 to 20 percent, which helped agencies expand counseling capacity and educational services on a broader scale.

This model helped build the field, but it also introduced an important structural question. Counseling agencies were expected to help consumers review budgets, understand options, and regain stability, while also operating within a funding system connected to creditor recovery. That dual character became one of the most discussed features of the industry.

Growth, pressure, and industry change

During the 1980s and early 1990s, credit card use expanded rapidly and demand for debt help increased with it. Debt management plan enrollments rose, and many counseling agencies extended their reach, staffing, and educational programming as more households sought assistance.

By the mid-1990s, however, the economics of the sector began to shift. Major creditors reduced fair share payments sharply, often pushing them into the single digits. That change placed substantial pressure on agencies that had long depended on creditor support to sustain operations.

The effect was significant. Smaller agencies found it harder to maintain traditional in-person models, consolidation increased, and larger organizations relied more heavily on centralized and phone-based counseling. In practical terms, the field became leaner, more operationally focused, and in some cases more dependent on scale.

This period also changed how consumers encountered debt-help services. As the marketplace grew more crowded, consumers were increasingly exposed to offerings that sounded similar on the surface but followed very different models in practice. That confusion helped set the stage for stronger distinctions and stronger regulation later on.

Why credit counseling is different from debt settlement

Nonprofit credit counseling and debt settlement are not the same service. Traditional credit counseling focuses on budget review, financial education, and, when appropriate, debt management plans designed to repay the full principal balance over time under modified terms.

Debt settlement generally follows a different approach. Rather than emphasizing full repayment over time, settlement programs often center on trying to negotiate a reduced payoff after a period of nonpayment. That process can involve added credit score damage, collection activity, and lawsuit risk while accounts remain delinquent.

The distinction became increasingly important in the late 1990s and early 2000s, when some debt-relief operators used nonprofit status or nonprofit-style language in ways that did not match the public’s expectations of a charitable counseling organization. In 2003, the report Credit Counseling in Crisis helped bring national attention to conflicts of interest, aggressive market entrants, and the blurred lines between education-focused counseling and other debt-relief models.

By 1997, clearer disclosure of creditor funding had already become a major issue. NFCC member agencies were required to inform consumers in writing that they received substantial support from the same creditors with whom they negotiated. That did not eliminate the counseling model, but it did make transparency a more visible part of the public conversation.

Looking for the present-day version? See how nonprofit credit counseling works and how a debt management plan works.

The regulatory turning point

The years from 2005 to 2010 were a major turning point for the field. In 2005, the Bankruptcy Abuse Prevention and Consumer Protection Act made pre-filing counseling from an approved nonprofit agency a requirement for most individual bankruptcy filers. It also added a post-filing financial management education step before discharge.

This change gave approved counseling agencies a more formal place within the bankruptcy process and increased the importance of federal approval standards. It also reinforced the expectation that counseling agencies would operate within a more structured compliance environment than in earlier decades.

The Pension Protection Act of 2006 tightened expectations for tax-exempt credit counseling agencies and reinforced that nonprofit status required more than simply adopting the label. Federal scrutiny increased, and standards related to governance, individualized service, and charitable purpose became more explicit.

At the same time, the legal and regulatory environment around credit repair and debt settlement also tightened. In 2010, the Federal Trade Commission amended the Telemarketing Sales Rule to prohibit advance fees for debt settlement services before a successful result had been achieved. That helped draw a clearer line between nonprofit counseling and higher-risk debt-relief models that relied heavily on upfront-fee structures.

What this history means today

Today, credit counseling exists in a more regulated and more clearly defined environment than it did a generation ago. Agencies must navigate state requirements, bankruptcy-related approval standards, consumer-protection expectations, disclosure practices, and continued public scrutiny.

At the same time, the need for guidance has not diminished. Consumers now face not only credit cards and traditional loans, but also digital lending, debt settlement advertising, credit-repair claims, and newer products such as buy now, pay later arrangements. The products may look different, but the underlying need for clear financial analysis and trustworthy education remains.

This history also explains why consumers are often advised to look carefully at how a service is structured. Two companies may both promise debt help, but the underlying methods, risks, costs, and outcomes can differ substantially. That is one reason nonprofit counseling continues to emphasize education, budget review, and informed decision-making rather than quick claims or broad promises.

Money Fit is one contemporary nonprofit participant in that longer history. Like other legitimate counseling organizations, it operates in a field shaped by consumer need, operational reform, and decades of regulatory clarification.

Common questions

Did credit counseling begin as a government program?

No. Organized credit counseling grew largely through efforts inside the consumer credit system itself, especially as lenders and communities looked for more coordinated ways to respond to delinquency, default, and bankruptcy risk.

What is fair share?

Fair share is a historical funding model in which participating creditors voluntarily returned a percentage of recovered funds to counseling agencies. It helped support nonprofit counseling services for many years and also raised important questions about incentives, independence, and transparency.

Is a debt management plan the same as debt settlement?

No. A debt management plan generally aims to repay the full principal balance over time under modified terms. Debt settlement usually aims to negotiate a reduced payoff after a period of nonpayment, which can carry added legal, credit, and collection risks.

Why did the field become more regulated?

Regulation increased as the debt-help marketplace became more crowded and more difficult for consumers to evaluate. Lawmakers and regulators worked to create clearer distinctions between legitimate nonprofit counseling, credit repair, and riskier debt-relief models, while also tightening standards for nonprofit operations and consumer disclosures.

Where to go from here

If you are exploring your options, it can help to start with a clear understanding of how nonprofit credit counseling works today and how it differs from other forms of debt relief. Knowing the history will not solve a debt problem by itself, but it can make the modern debt-help landscape easier to evaluate and easier to navigate.

Last reviewed: March, 2026 | URL: /history-of-credit-counseling/