Loans & Borrowing How-to Guide

How to Avoid Payday & High-Interest Loans

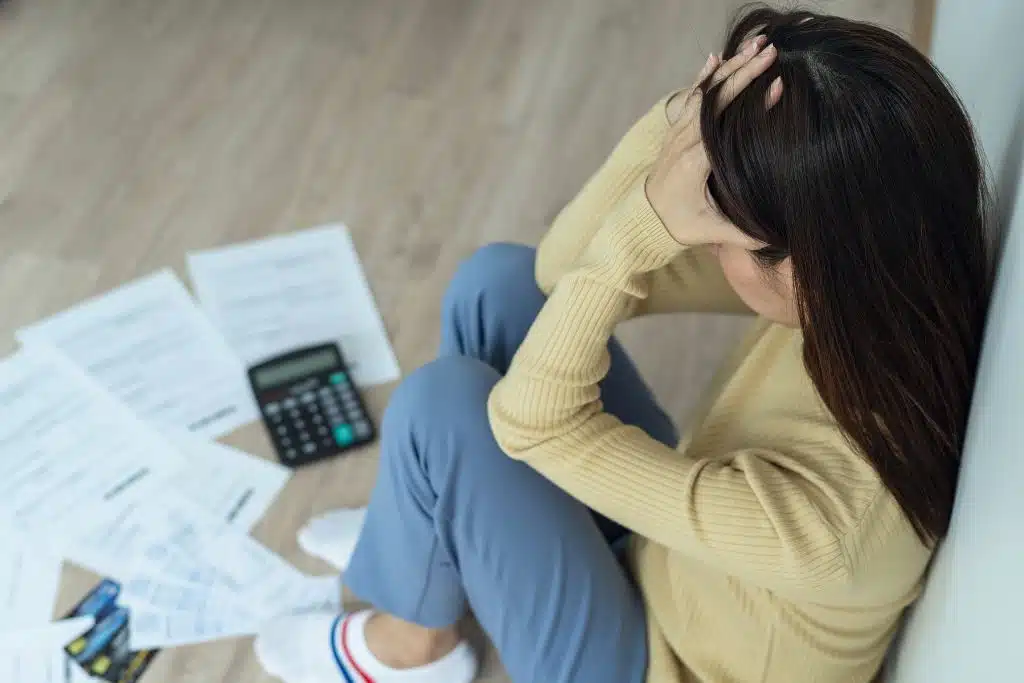

Payday loans and other high-interest loans can be expensive because repayment is often due quickly and fees can turn a small short-term loan into a much larger budget problem. Before borrowing, slow the decision down, calculate the full cost, and look for safer ways to handle the cash shortfall.

Where to start

To avoid payday and high-interest loans, first write down the exact amount you need, the date it is due, and what will happen if you cannot pay it on time. Then calculate the full cost of any loan, including fees, APR, repayment date, rollover or renewal costs, and whether the lender can access your bank account. Before borrowing, ask creditors for more time, compare credit union or small-dollar loan options, review community resources, consider employer or hardship assistance, and talk with a nonprofit credit counselor if debt payments are driving the need for another loan.

A high-cost loan may solve a deadline today while making the next paycheck harder to live on. The goal is to handle the immediate need without creating a larger repayment problem.

Quick facts about payday and high-interest loans

Payday loans can be costly because the repayment window is short and fees can be high compared with the amount borrowed.

How to avoid payday and high-interest loans step by step

The first job is to understand the emergency clearly enough that you do not buy a more expensive problem.

-

Name the exact shortfall

Write down the amount you need, the deadline, who needs to be paid, and what will happen if the payment is late. This helps separate urgent needs from pressure or panic.

-

Calculate the full loan cost

Look at the fee, APR, repayment amount, repayment date, rollover or renewal rules, late fees, and what happens if you cannot pay on time.

-

Check whether the lender wants bank account access

Review whether the lender requires automatic electronic payments, debit card access, postdated checks, or other repayment access. Ask what happens if the payment fails.

-

Ask the biller or creditor for time

Before borrowing, ask whether the landlord, utility, medical provider, creditor, or service provider offers a payment plan, due-date change, hardship option, extension, or partial-payment arrangement.

-

Compare lower-cost borrowing options

Check credit unions, small-dollar loans, payday alternative loans where available, employer assistance, family support if safe and appropriate, and existing credit only if the repayment cost is clear.

-

Look for community resources

Local nonprofits, community action agencies, churches, housing programs, food assistance, utility assistance, and medical hardship programs may reduce the amount you need to borrow.

-

Review the budget behind the emergency

If the same shortfall keeps returning, look at income timing, debt payments, subscriptions, insurance, transportation, groceries, and irregular expenses. The issue may be structural, not just temporary.

-

Talk with a nonprofit credit counselor if debt is driving the need

If credit cards, medical bills, collections, or other unsecured debts are crowding out essentials, a nonprofit credit counselor can help review the full picture and discuss possible next steps.

Alternatives to check before a payday loan

Not every option will be available to every person. The point is to check lower-cost and lower-risk paths before agreeing to expensive short-term borrowing.

Payment plan

Ask the biller whether you can split the amount, change the due date, pay part now, or avoid a late fee through an arrangement.

Credit union loan

Some credit unions offer small-dollar loans or payday alternative loans with lower costs than many payday loans.

Community help

Local programs may help with food, utilities, rent, transportation, prescriptions, or emergency needs.

Employer assistance

Some employers offer payroll advances, emergency assistance, employee hardship funds, or earned wage access. Check fees and repayment timing.

Hardship programs

Creditors, lenders, medical providers, utilities, and servicers may have hardship options, especially if you contact them early.

Nonprofit credit counseling

If debt payments are the reason money is short, counseling can help review income, expenses, debts, and possible paths forward.

If you already have a payday loan

Start by getting organized. A loan already taken out still needs a careful plan, especially if repayment will leave the next paycheck short.

Write down the repayment date

Include the loan amount, fee, total due, lender name, payment method, and whether the lender can withdraw from your account.

Ask about repayment options

Ask the lender what happens if you cannot pay in full and whether any extended payment plan or state-specific option may apply.

Protect essential bills

Map the repayment against rent, utilities, food, transportation, medicine, and required payments before the due date arrives.

Get help before rolling it over

If repayment would require another loan, pause and review alternatives, creditor arrangements, community resources, or nonprofit counseling.

Be careful with automatic withdrawals

Some high-cost loans involve automatic electronic payments from your bank account. That can create added stress if the lender tries to withdraw money when the balance is too low.

CFPB provides consumer information on stopping payday lender electronic payment withdrawals and explains common payday loan issues. If you are dealing with automatic withdrawals, use official guidance and communicate with your bank or credit union promptly.

- Know the payment date. Do not rely on memory when automatic withdrawals are involved.

- Watch the account balance. A failed payment may create lender fees, bank fees, or both.

- Use official contact information. Contact the lender and your bank through verified channels.

- Keep records. Save emails, letters, payment confirmations, cancellation requests, and bank messages.

Official payday loan resources worth checking

These official sources can help you understand payday loan costs, alternatives, and common consumer issues before making a decision.

CFPB: What is a payday loan?

Explains how payday loans work and why common fees can equal a very high APR on a short-term loan.

CFPB: Payday loan costs and fees

Explains common payday loan fees and gives an example of how a two-week loan can reach an APR of almost 400 percent.

CFPB payday loan resources

Covers payday loan rights, common issues, repayment problems, and electronic payment concerns.

FTC: Payday and car title loans

Provides consumer guidance on payday and car title loans, including possible alternatives to check first.

Common mistakes to avoid

Payday loans and high-interest loans often become more difficult when the repayment plan is not clear before signing.

- Looking only at the dollar fee. A fee that looks small can be expensive when the loan is only for a week or two.

- Ignoring the next paycheck. A loan due on payday can leave too little for rent, food, transportation, utilities, or other bills.

- Letting repayment access go unchecked. Know whether the lender can withdraw from your bank account and what happens if the payment fails.

- Rolling the loan forward without a plan. Renewals, rollovers, or repeat borrowing can increase the total cost.

- Borrowing to pay another short-term loan. Replacing one expensive loan with another can keep the same problem alive.

- Waiting to ask for help. Creditors, utility providers, landlords, medical providers, and nonprofit counselors may have more options before the due date passes.

The problem is usually the next paycheck

Money Fit often sees that payday loans are used when someone is trying to keep the lights on, get to work, cover medicine, or stop a bill from falling further behind. That pressure is real.

The danger is that the repayment may arrive before the household has recovered. If the next paycheck is already promised to the lender, the same shortage can return with less room to solve it. That is why the budget behind the emergency matters as much as the loan itself.

Review the budget and debt pressure first

If payday loans, credit cards, collections, medical bills, or other unsecured debts are making it hard to cover essentials, a Money Fit nonprofit credit counselor can help you review income, expenses, debts, and possible next steps. A debt management plan may be one option for some eligible unsecured debts, but it is not a loan, not debt settlement, and not a guaranteed fit for every situation.

Frequently asked questions

Why are payday loans so expensive?

Payday loans are often due quickly and may charge a fee for every amount borrowed. When that short-term fee is shown as an annual percentage rate, the APR can be very high.

What should I do before taking out a payday loan?

Calculate the full repayment amount, due date, fees, APR, rollover rules, and what happens if you cannot pay on time. Then check payment plans, creditor hardship options, credit union loans, community resources, and nonprofit credit counseling if debt is part of the problem.

Are payday alternative loans better?

Payday alternative loans from federal credit unions may be less expensive than many payday loans, but eligibility, fees, loan limits, and repayment rules still matter. Read the terms before borrowing.

Can a payday lender take money from my bank account?

Some payday lenders ask for authorization to collect payment electronically from your bank account. Review the authorization carefully, keep records, and contact your bank or credit union quickly if there is a payment problem.

What if I already have a payday loan I cannot repay?

Contact the lender to ask about repayment options, review your state rules, protect essential bills, and avoid taking another high-cost loan without checking alternatives. A nonprofit credit counselor can also help review the full budget and unsecured debt picture.

Can Money Fit help with payday loan debt?

Money Fit can help review your income, expenses, unsecured debts, and possible next steps. Payday loans may need separate handling depending on the lender, state rules, account status, and loan terms. Money Fit will tell you if a program is not a good fit.

About the author

Rick Munster is Senior Manager of Compliance & Media at Money Fit, with more than two decades of experience in nonprofit credit counseling, financial education, compliance, and consumer-focused content. He also serves on the Board of Directors of the Financial Counseling Association of America.