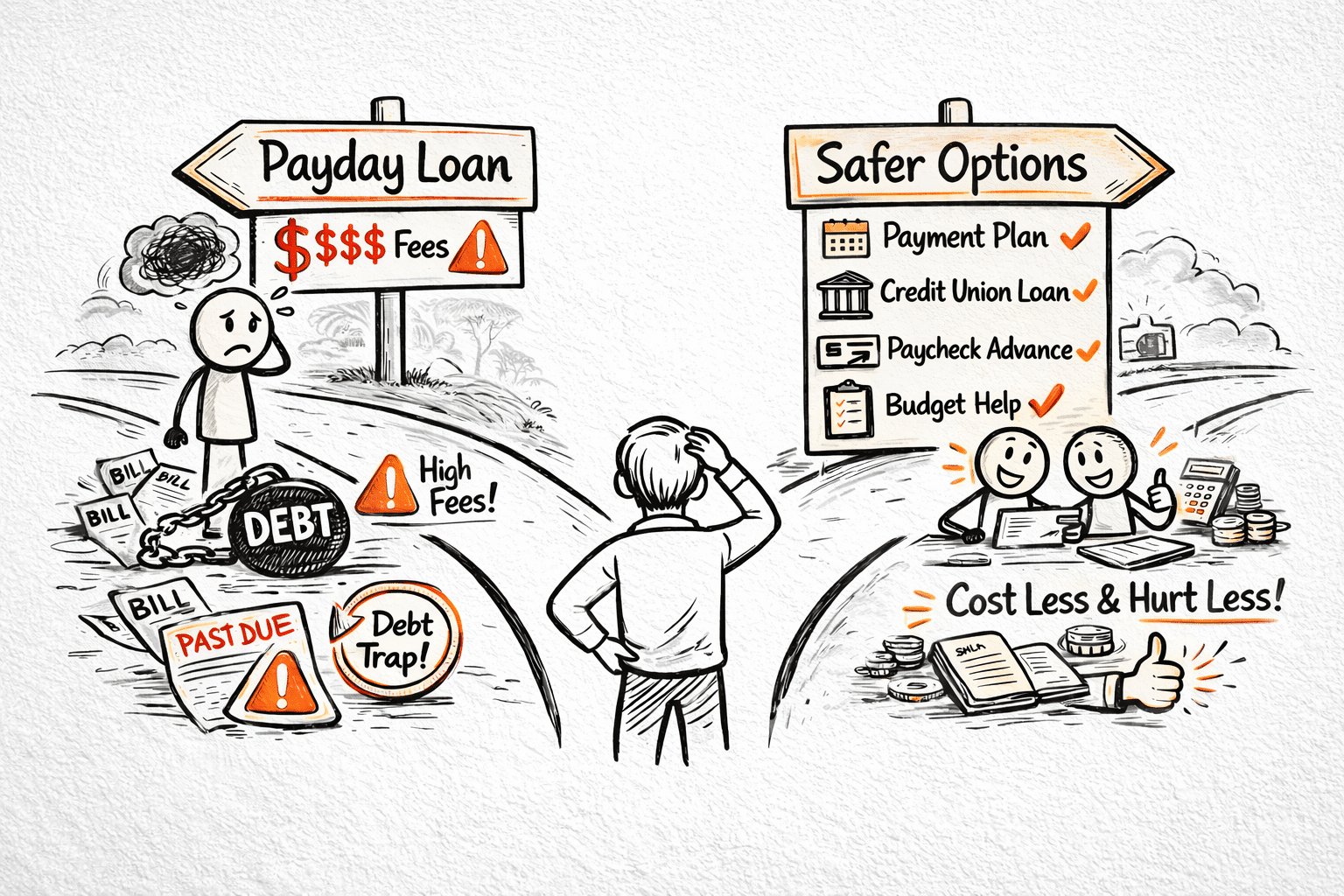

Your Options Beyond a Payday Loan

When money runs short and a bill cannot wait, a payday loan can look like a quick answer. The problem is that quick answers often come with long consequences. What starts as a short-term cash gap can turn into repeated fees, another loan, and a cycle that gets harder to escape each time.

That does not mean every person facing a cash shortage has good options lying around. Sometimes the situation is urgent. Rent is due. Utilities are at risk. The car needs repair so you can get to work. In moments like that, people do not need judgment. They need a clear look at what may cost less, hurt less, and create fewer problems a month from now.

If you are trying to avoid another payday loan, or you are thinking about one because you feel cornered, slow the process down just enough to compare your options. The best choice may still be difficult, but it does not have to be the most expensive or the most damaging.

Why payday loans are hard to escape

Payday loans are built for speed, not stability. They are often easy to get, but that ease comes at a price. High fees, very short repayment windows, and rollover pressure can leave people borrowing again just to stay afloat.

The real risk is not just the cost of one loan. It is what happens next. If repaying the loan leaves you short on groceries, utilities, rent, or gas, the same emergency can show up all over again. That is how a short-term fix becomes a repeated drain on the budget.

This is why it helps to ask a different question. Not just, “How do I get cash today?” but, “What can solve this problem with the least long-term damage?” That question usually leads to better choices.

Quick Wins Box

- Pause before accepting the first fast-cash offer you see

- Write down exactly how much money you need and when you need it

- Separate urgent bills from bills that may have some flexibility

- Compare total cost, not just how quickly the money arrives

What to do before you borrow

Before comparing lenders or applications, take ten minutes and get clear on the problem in front of you. A smaller, more exact need is often easier to solve than a general feeling of financial panic.

- What bill or expense is creating the emergency?

- How much money do you actually need to get through it?

- Is the deadline fixed, or can you ask for more time?

- Could part of the problem be solved without new borrowing?

- Will taking a loan create another shortfall next paycheck?

In many cases, the first safer alternative is not a loan at all. It may be a payment extension, a due-date shift, a split payment arrangement, or a temporary hardship conversation with the company you owe. That is not always possible, but it is worth checking before you sign up for high-cost debt.

Mini-Scenario

If you need $300 for a utility bill, the best move may not be borrowing $500 because that is what a lender offers. It may be calling the utility company, explaining the situation, and finding out whether a partial payment can keep the service on. The fastest money is not always the smartest answer.

Safer alternatives to payday loans

No option is perfect when money is already tight. Still, some choices are clearly less harmful than others. The alternatives below are worth checking before you commit to a payday loan.

1. Ask for more time from the biller

This may be the most overlooked option. Landlords, utility companies, medical providers, and even some lenders may allow a payment arrangement, partial payment, or due-date extension. Not every request will be approved, but a short conversation can sometimes solve the immediate problem without adding new debt.

If the expense is urgent, start there. Be direct. Ask what keeps the account in the best standing possible. Ask whether there is a hardship option or a short-term arrangement. Get any agreement in writing when you can.

2. Look into a credit union small-dollar loan

Some credit unions offer smaller loans with clearer terms and lower costs than payday lenders. These are not free, and you still need to repay them, but they may provide a safer structure for someone who needs short-term help.

The key is to look closely at the total repayment amount, any fees, and whether the payment fits your next few weeks of cash flow. A smaller loan with reasonable terms is still only helpful if it does not throw your next paycheck into chaos.

3. Explore an employer paycheck advance carefully

Some employers offer paycheck advances or earned wage access programs. In the right situation, this may be less costly than a payday loan because you are accessing income you have already earned rather than taking on a separate high-fee debt product.

Still, it is smart to read the details. Some services include fees, tips, subscriptions, or timing structures that can quietly add up. A lower-cost option is still worth comparing, not blindly trusting.

4. Consider an installment loan with clear terms

An installment loan can be safer than a payday loan if the terms are transparent, the total cost is reasonable, and the payments fit your budget. The danger is assuming every installment loan is automatically better. Some still carry high costs and can create a long repayment burden for a short-term problem.

Before agreeing to one, check:

- The total amount you will repay

- Any origination or extra fees

- The exact monthly payment

- How long repayment lasts

- What happens if you miss a payment

If the structure is clearer but the total damage is still heavy, it may not be the right answer.

5. Sell, pause, or cut something before borrowing more

This is not always enough on its own, but it can shrink the problem. Selling an unused item, delaying a nonessential expense, pausing subscriptions, or cutting a discretionary purchase for one pay cycle may reduce how much you need to borrow in the first place.

That matters because the safest loan is often the smaller loan. And sometimes the smaller loan becomes no loan at all.

6. Nonprofit credit counseling

If short-term borrowing has become a repeated pattern, the issue may be bigger than one emergency. Nonprofit credit counseling can help you look at the full picture, review your budget, and sort out whether the real problem is high-interest debt, unstable cash flow, or a combination of both.

This is especially useful when payday loans are not the only strain in the budget. If credit card balances, medical bills, or other unsecured debt are also crowding out your income, counseling may help you find a steadier path instead of another temporary patch.

To learn more, see what to expect from credit counseling and options for dealing with payday loan pressure.

How to compare short-term borrowing options

When people are stressed, they often compare offers by speed alone. That is understandable, but it can be costly. A better comparison comes down to four things.

- Total cost: How much money will leave your pocket by the end?

- Repayment pressure: Will paying this back create another shortage right away?

- Clarity: Are the fees, timeline, and consequences easy to understand?

- Repeat risk: Does this option make it more likely you will need another loan soon?

A slightly slower option with lower cost and less rollover risk may be much safer than instant cash with a brutal repayment timeline. The goal is not just solving today. It is protecting next week too.

Future-You Snapshot

A month from now, the best decision may not be the one that felt easiest in the moment. It may be the one that kept one emergency from becoming three more. Short-term relief matters, but so does leaving yourself enough room to breathe after the crisis passes.

Warning signs that an option may be too risky

Some products are designed to sound friendly while hiding the true cost. Slow down if you see any of these warning signs:

- The lender focuses on speed but avoids talking clearly about total cost

- Fees are hard to find or explained in vague language

- You are encouraged to borrow more than you actually need

- The repayment date is unrealistically close to your next major bills

- The offer seems to depend on repeat borrowing

- You feel rushed to agree before you fully understand the terms

When an option creates confusion, pressure, or a high chance of repeat borrowing, that is usually a bad sign. Real help should be understandable. Even in an emergency, you deserve clear terms.

A simple 30-day reset after a cash crunch

If you have just made it through a tight stretch, use the next month to reduce the odds of ending up in the same place again.

Week 1

- List the bill or event that caused the shortage

- Write down what you borrowed, or almost borrowed, and why

- Review which expenses were truly fixed and which had some flexibility

Week 2

- Look for one or two expenses you can trim temporarily

- Set aside even a small buffer for the next surprise expense

- Review whether high-interest debt is making every month tighter

Week 3

- Call any creditors that may offer hardship help or due-date changes

- Compare safer borrowing options before another emergency appears

- Write down a short list of “better than payday” choices for next time

Week 4

- Build a simple emergency plan for bills, transportation, and essentials

- Update your budget with one realistic change you can maintain

- Get outside help if the problem is becoming a pattern

If budgeting is part of the challenge, see How to Budget for a practical place to begin.

When this is really a debt problem, not just a cash problem

Sometimes a payday loan is the symptom, not the core issue. If your budget is already crowded by credit cards, collections, or other unsecured debt, then one short-term emergency can push everything over the edge. In that case, the answer may not be a different small loan. It may be a broader plan to reduce pressure across the whole budget.

If that sounds familiar, it may help to read How to Get Help With Credit Card Debt and how a Debt Management Plan works.

Final thoughts on payday loan alternatives

When money is tight, there may not be a perfect answer. But there is often a less damaging one. Before taking on another payday loan, look at whether more time, a smaller need, a lower-cost option, or a broader financial plan could solve the problem with fewer consequences.

You do not need a flashy promise. You need the least harmful path you can realistically sustain. In moments like this, steadier is usually better.